Managing the Federal Balance Sheet: The Allure of Loan Sales

The idea of monetizing the federal government’s massive credit portfolio by selling government-held loans into the market surfaces periodically. Loan asset sales have several features attractive to policymakers. They bring in private capital to support areas traditionally served by government programs. They take risk off the government’s balance sheet. They can also appear to offer a near-term budgetary gain, since the government is receiving an upfront lump sum in exchange for an (uncertain) future cash flow stream. But while the first two benefits are real the third is illusory, at least under current budgeting rules.

Loan asset sales have several features attractive to policymakers. They bring in private capital to support areas traditionally served by government programs. They take risk off the government’s balance sheet. They can also appear to offer a near-term budgetary gain, since the government is receiving an upfront lump sum in exchange for an (uncertain) future cash flow stream. But while the first two benefits are real the third is illusory, at least under current budgeting rules.

If federal leaders are to seriously consider loan asset sales as a policy approach, they must understand the budget rules that drive their feasibility. The key points are:

- The Federal Credit Reform Act (FCRA) governs budgeting, accounting, and valuation of government loans and loan guarantees.

- Selling government-held loans to private sector buyers is difficult because market values—and therefore sale prices– are almost always less than the government’s FCRA carrying value. This generates a budgetary cost and this cost must be paid for.

- If a loan program incorporates loan sales into its design, loan sale costs can be budgeted upfront. While this enables loan sales, it raises subsidy costs and tends to reduce program lending volumes. If not budgeted upfront, loan sales require appropriations at the time of sale.

- Were Fair Value (FV) budgeting to be adopted, loan sales would be greatly enabled as government carrying values would converge to market values, reducing or eliminating budgetary losses. FV would have the effect of increasing the government’s cost of credit generally.

FCRA Background

The Federal Credit Reform Act of 1990 (FCRA) governs how credit agencies budget and account for loan and loan guarantee programs. FCRA took effect in FY 1992, for all credit commitments made from that point forward.

Under FCRA, the budgetary cost of extending credit (“credit subsidy cost”) is the net present value (NPV) of that credit’s expected lifetime cash inflows and outflows. Agencies forecast cash flows, then discount them at US Treasury rates. Administrative costs are excluded from this calculation.

After making a loan or guarantee, a government agency carries that asset (or liability) on its balance sheet at the NPV of future cash flows. Discounting continues to be performed using Treasury rates.

The Challenge

Because US Treasury rates are “risk-free”, the government’s carrying value for loan assets (Value to Government) is nearly always higher than the amount for which those loan assets could be sold in the market (Market Value), since market participants incorporate risk into their valuations and the prices they pay.[1] Exceptions to this may occur, for example when the government’s view of expected future cash collections is substantially lower than those of private sector buyer’s.

When the Value to Government is higher than the Market Value, selling a government loan asset to a private party would result in a loss and an appropriation would be required to cover the cost.[2] When budget resources are scarce, this makes it hard to sell government loans to private parties.

The Potential Impact of Fair Value

There have been periodic efforts to replace FCRA with Fair Value (FV) credit budgeting. Under FV budgeting, the cost of extending loans and loan guarantees would take into account market risks. With FV, the government’s budgetary cost to extend credit would increase and its carrying values for loans and loan guarantees would mirror market values. If the government carries loan assets at market values, selling those loans at market would be budget neutral.

Enacting FV would require legislation. Such legislation could be government-wide, as proposed in the Budget and Accounting Transparency Act of 2015, or it could be specific to a program, as it was for the Troubled Asset Relief Program.[3]

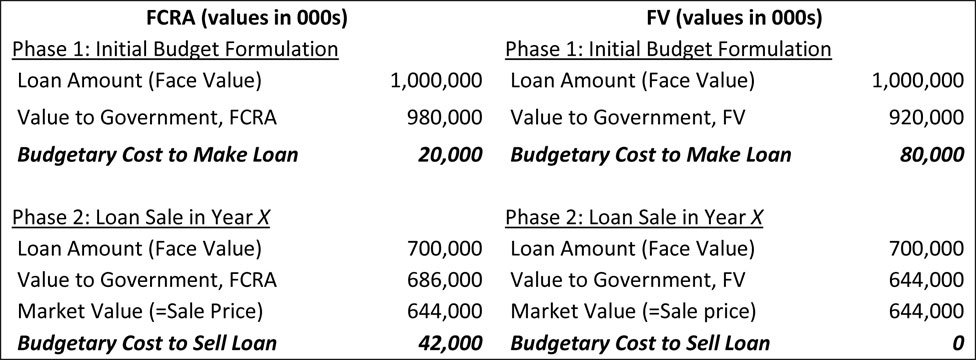

An Example

The example below illustrates the budget implications of a hypothetical loan sale scenario using FCRA and FV budgeting. The key difference to focus on is in the timing of when budget appropriations are required.

Room to Maneuver within FCRA

Room to Maneuver within FCRA

There is room within the existing FCRA budgeting framework to better enable loan asset sales. Incorporating expected future loan sales into upfront estimates recognizes the cost of loan asset sales upfront. This increases budget requirements but avoids the need for a modification (and an appropriation) later. This approach can only work for new loan cohorts.

[1] The same principle holds for loan guarantees—the government would have to pay a private party more than the amount of the government’s liability to transfer the risk.

[2] The exception to this is if the loan asset sale was explicitly accounted for in the original budget formulation.

[3] The Troubled Asset Relief Program was statutorily required by EESA to discount its cash flow forecasts using “market-adjusted discount rates”, a Fair Value approach.